The Real Yield narrative

The Real Yield narrative

A complete article about the Real Yield narrative, one of the hottest sectors of the moment

Overview

The real yield narrative has been on everyone's mind over the last few months, many people are making money out of it, and some of these projects are breaking their ATH week after week. And for a good reason: projects that have included a real yield mechanism in their tokenomics offer one of our sector's most innovative operating systems, creating a natural virtuous circle for all participants in these protocols.

However, at this stage, the question to ask is:

Is this narrative an ephemeral hype without real interest, or does it represent a new paradigm for crypto?

This is the question we will try to answer today. To do so, let's dive deeper into this exciting domain and understand its functioning.

In this article, we will see the following:

I/ The main issues of the first DeFi wave of 2020 - 2021

II/ What are Real Yield protocols

III/ The virtuous circle of this mechanism

IV/ How to find and analyze these projects

V/ The two main sectors affected by this innovation and the leading projects

VI/ Starknet projects that will (or should) include this mechanism

I/ The main issues of the first DeFi wave of 2020 - 2021

The DeFi boom of 2020 created many innovative protocols and began the DeFi market we know today. Protocols such as @Uniswap, @SushiSwap, @MakerDAO, @iearnfinance, @AaveAave, and @compoundfinance pioneered this disruptive innovation and are still some of the most significant DeFi protocols to date.

However, as with any nascent market and to compete, the protocols have embarked on numerous experiments to attract user attention and capital. This resulted in a wild race to attract TVL and protocols offering insane APY to catch it. These high APY came mainly from highly inflationary liquidity mining or yield farming mechanisms, ultimately creating unsustainable APY. This means that liquidity providers were rewarded by receiving the newly created tokens from the protocols, which poses many problems.

Let's take the Compound’s example to understand:

This protocol generated an average monthly income of $1M5 between February and June 2021. An impressive revenue, which could demonstrate the financial strength of the protocol. In reality, not really, because when you subtract the revenue generated by the protocol with the value of the crypto created paid back to the liquidity providers, you can see that the platform was actually loss-making:

An average dry loss of $1M per month over the same period, a significant capital inefficiency.

In addition, this liquidity mining offering these unsustainable APY creates a vicious circle for the protocols that set it up:

Protocols attract 'bad' users, who take advantage of the insane APY, dump the tokens they receive and move on to a new protocol offering better APY

Investors who believe in the protocol's future and invest in the token lose money, as the selling pressure of liquidity mining is too significant on the token

These investors lose faith in the protocol, dump the token and leave the project

As a result, we end up with many DeFi protocols whose TVL has melted like snow in the sun and investors/users who lose interest in the project. As no incentive to participate in the project's development is provided, the demand for the protocol drops while the supply of tokens continues to grow, resulting in what is commonly known as dump tokens.

Is there a better way to reward liquidity providers and protocol stakeholders? The answer is yes, through the Real Yield mechanism.

II/ What are Real Yield protocols

A Real Yield protocol is a DeFi protocol that generates real revenue and distributes this revenue to the platform's token holders and liquidity providers. This revenue is generated from fees that the protocols charge to users who use their services, such as:

Fees on opening and closing a Perp trade

Fees on Swap

Fees for buying and selling NFTs

Fees for holding an ETH domain name

We call it real revenue because users are willing to spend capital (such as stablecoins or ETH) to access the protocol services. This revenue is then redistributed to the protocol stakeholders (token holders, LP, and sometimes the DAO). Holders and liquidity providers are thus rewarded with real revenue rather than artificial revenue creation, which finally destroys their holding value.

It is important to note that most real yield protocols also distribute a % boost of their Yield in project tokens.

But, a large part of them offer this liquidity mining with:

a) a sustainable inflation

b) a mechanism to make the holding interesting

c) a smart and innovative way of distributing new tokens

Taking the GMX example:

a) The circulating supply is 8,453,965 for a max supply of 13,250,000, more than 63% of the supply already issued on the market. The token inflation is less than 20% per year, reducing selling pressure while incentivizing stakers and LPs.

b) GMX token holders have governance rights over the protocol but are especially entitled to receive 30% of the revenues/fees generated by the protocol when they stake (without locking) their tokens. These revenues are distributed in ETH (for the Arbitrum chain) and AVAX (for the Avalanche chain). In addition to these revenues, they receive esGMX and Point Multipliers that boost their APR.

c) GMX token inflation is not in the form of newly created and liquid GMX but in the form of esGMX (escrow GMX). These esGMX can either be staked to get the same rewards as a normal GMX, i.e., ETH/AVAX, MP, and esGMX, or they can be vested to become normal GMX linearly after one year.

The beauty of this mechanism is that :

When a user unstakes his GMX, he loses its MP (in proportion to the GMX he withdraws)

When a user wants to transform an esGMX into a GMX, he must hold and stake the equivalent GMX that allowed him to obtain this esGMX and place the esGMX in a vault. esGMX tokens that have been unstaked and deposited for vesting will not earn rewards.

GMX holders are therefore incentivized to hold their GMX and compound their rewards.

In short, a real yield project includes :

A real use

A real service that meets a real need

Users who are willing to spend real capital to use the project's services

Redistribution of these fees (in part or entirely) to the platform's stakeholders

Using GMX example:

Real use? Yes, clearly:

A real service that meets a real need? Yes, GMX offers non-custodial and permissionless trading of Perp and spot. In addition, it allows anyone to bring liquidity to an exchange and become a 'shareholder' of that exchange.

Users who are willing to spend real money to use the project's services? Yes, GMX is one of the top 5 projects collecting the most fees in the entire crypto ecosystem -≥ https://cryptofees.info

Any redistribution of these fees to the platform’s stakeholders? Yes, 30% is paid to GMX stakers and 70% to liquidity providers.

I am personally an early investor and holder of GMX, but I really became aware of the magnitude of the Real Yield narrative thanks to two articles that I highly recommend you read:

III/ The virtuous circle of this mechanism

The Real Yield mechanism creates a natural virtuous circle around the projects that use it:

Traders are interested in trading on this kind of platform (especially since the FTX incident) because they offer non-custodial and permissionless trading; the only clear disadvantage so far is that the fees are higher than on CEX.

These traders have an interest in holding the platform's token to recoup some of the fees they pay and also to gain exposure to the growth of the protocol they are trading on (if the protocol in question sucked, they wouldn't come to trade on it, so they recognize the added value of the protocol). Some platforms even offer a reduced fee for token holders, such as dYdX.

Token holders have a direct interest in the success of the protocol because the more the protocol is known, the more traders will trade on it, the more volume will increase, the more fees they will receive, and the more the token in question will be undervalued and the more it will progress. So it is in their interest to do community marketing for the protocol to earn more fees and see their holding increase in value.

They even have the incentive to trade on the platform rather than with competitors, as this will improve the platform's metrics, and they will receive more fees.

In short, traders have a vested interest in trading on these platforms and also holding the token of these platforms. Holders are directly interested in making the platform known and trading on it. Wonderful, isn't it?

This kind of platform changes the paradigm from 'in for the tech' to 'in for the yield' (s/o DeFiMann for the quote). Let's take Arthur Hayes' example on GMX and the superb analyses of Lookonchain and DeFiMann to illustrate this principle.

Arthur Hayes bought 200,580 GMX for a total acquisition cost of $5.72M between March and September 2022 (an average price of $28.5). As of February 6, he has already acquired as a reward :

344.5 ETH (or $558,080)

12,405 esGMX ($818,744)

Therefore, without mentioning the upward evolution of the token, Arthur has already covered his initial investment by :

10% in liquid ETH rewards

15% in esGMX (locked rewards which unlocks linearly over 1 year under certain conditions)

So, in terms of yield rewards alone, Arthur repaid 25% of his investment in less than a year.

Despite this, he is not selling anything and is compounding his rewards. Why does he do this? Simply because, unlike traditional liquidity mining on a single governance token, GMX introduces many incentives to hold and stake the token:

staked GMX produce esGMX and MP

esGMX produce the same rewards as GMX but are not sellable; to be able to sell them, you have to place them in a vault for 1 year (which will not produce rewards) and stake the GMX that produce these esGMX

MP produce a yield boost and allow you to have the same yield as a GMX (a GMX gets 1 MP after 1 year of staking), but destaking a GMX leads to the destruction of the MP it produced

In short, the longer GMX holders stake their GMX and rewards, the larger the share of the GMX fee they get. Here are the top 10 GMX staking addresses:

Our dear Arthur earns 2.381% of the fees generated by the platform, and we can see that the biggest holders hold their GMX for a long period (referring to their MP boost).

Do you see the difference with classic liquidity mining on a token without real use?

In addition to this strong incentive to hold and stake the token, the exciting thing is that these kinds of platforms are only at the beginning of their growth phase:

Crypto is still very small and unknown to the general public compared to the traditional sectors

The DeFi sector is tiny compared to the centralized crypto services

The Real Yield field is still in its infancy compared to the entire DeFi market

IV/ How to find and analyze these projects

In my opinion, Real Yield is one of the most accessible domains to monitor and analyze. It is, therefore, easy to follow this trend and take advantage of it.

Here is Arthur Hayes' method to find Real Yield projects:

The website he talks about is Token Terminal, which gives you all the metrics, charts, and ratios you need to analyze these projects.

The most important metrics are:

The MC of the project

The fully diluted MC (you have to do some research about the token release schedule and how it is released)

The volume the project generates

The revenue that the project distributes to holders (and especially ask yourself if the protocol redistributes its revenues; for example, for OpenSea and dYdX, the answer is no)

The P/E (which is a ratio calculating the price of a crypto compared to what it brings in revenue to its holders)

One way to analyze this is the one presented by Arthur Hayes in the essay I quoted above: at the depths of the 2008 crisis, he showed that the world's two largest stock markets (CME and ICE) were negotiating around a P/E of 10 before rising to between 30 and 40 at the peak of 2022. Therefore, he considers an equivalent or lower P/E an attractive buying opportunity.

You can compare the P/E of the leading crypto projects in this narrative from this base while asking yourself the following question:

Is the project in a sector that has a high growth propensity?

Does the project offer a real service that meets real needs?

Where do the revenues come from, and is the collection model sustainable in the long run?

Does the protocol distribute some or all of its revenues to the platform's stakeholders (notably the token holders)?

Token Terminal does not list all Real Yield projects. To go further, you will have to find them by yourself, thanks to tools like Tweetdeck (here is a tutorial by Louround on how to use it) or simply by searching the keywords on Twitter's advanced search functions. Then, you will have to analyze by yourself the following :

Tokenomics

Calculate the metrics (most real yield protocols have a dashboard of important metrics directly on their dApp)

Their plan to improve their product and value proposition

And answer the questions above

Let's look at how to do this in the next section

V/ The two main sectors affected by this innovation and the leading projects

Disclaimer : note that my project presentations do not represent investment advice. Nor will I comment on future price evolution.

1) NFT marketplaces

The first area is the NFT market, specifically the NFT marketplaces. You are probably all familiar with the leading marketplace OpenSea, a pioneer in its value proposition, which generates over $150m in revenue per year:

This impressive figure can be explained by the fact that NFTs have become an asset class in their own right, which traders trade like traditional cryptos. We should therefore consider these platforms as the Binance of NFTs with the same business model: charging fees on all trades (purchases and sales) of NFTs. You know the famous story of the shovel sellers during the Gold Rush in America: we are in the same situation for NFTs and these marketplaces.

OpenSea's current revenues are impressive, but it should be noted that :

It generates these revenues in the middle of the Bear Market, during which there is an apparent disinterest in NFTs and crypto; I dare not imagine these figures in the middle of the Bull Market

Despite the 2021 boom, the NFT market is still in its infancy

This last point is especially true if we consider that more big players from the traditional sector are entering this market, producing their own NFT and offering associated services. The two most recent examples are the controversial launch of Donald Trump's NFTs and the Porsche NFTs.

In addition, there are many innovations in this field, and we have gone from simple JPEG avatars without any utility to NFTs with more and more services and exclusive content attached. This means that NFTs are becoming more and more attractive to own, leading to more and more volume on the NFT marketplaces.

Despite its impressive revenues, OpenSea is of no interest to us as investors: it has no token, so there is no way to gain exposure to the protocol's growth and recoup some of its revenues. However, two of the top 7 NFT platforms offer a similar service to OpenSea, with a token and a real yield system attached.

a) LooksRare

The first is LooksRare, a platform for selling and buying NFTs on ETH. It charges a 2% fee on each sale of NFTs, allowing it to generate an annualized revenue of about $27M.

The beauty here is that LooksRare redistributes 100% of the fees to LOOKS holders in ETH.

That is an APR of 21% (with more than 12.5% in Real Yield) at the time of writing (23 February 2023).

Furthermore, to take advantage of the NFT market growth and attract traders to its platform, LooksRare has implemented an incentive system where NFT traders receive newly created LOOKS, allowing them to cover part of the fees they pay.

The initial high inflation rate and the bear market caused the LOOKS price to collapse. However, 76.5% of the supply is currently liquid, and the inflation rate has decreased significantly.

Will the current low inflation of the token and the incentive to hold it be significant enough to maintain the token's price or even increase it?

I will not comment on this. But in my opinion, the virtuous circle around this token is mighty:

Traders have an interest in coming to trade on this platform because a part of their fees is refunded in LOOKS

It is not necessarily in their interest to sell the LOOKS at this price, especially if we take into account Arthur Hayes' investment theory about the P/E ratio of 10 (see the ratio below)

On the other hand, they have an interest in continuing to trade on LOOKS to recover part of their fees in newly issued LOOKS and significantly because, by staking their LOOKS, they recoup part of the total fees of the platform in ETH and accumulate even more LOOKS because of the staking rewards (8% APR in LOOKS in addition to the 13% in ETH)

Holders are interested in doing community marketing around LOOKS and trading their NFTs on it to improve the platform metrics and attract more people.

Regarding the current P/E of Looks, here it is

Circulating: 140M/27M = 5,18, the formula being (MC of Looks stake / annualized revenue)

Fully diluted: 235M/27M = 8,7, the formula being (Fully diluted MC / annualized revenue)

Finally, our four questions :

Is the project located in a sector with a high growth propensity? Yes, for the reasons I stated above (TLDR: bull market, the democratization of the NFT market, and innovation about the usefulness of NFT)

Does the project offer a real service that meets real needs? Yes, to be able to trade NFTs on a platform with deep liquidity, which is owned by its community and redistributes its revenues

Where do the revenues come from, and is the collection model sustainable in the long run? The protocol charges a 2% fee on NFT sales, which is the average in the NFT market, so the viability is there

Does the protocol distribute some or all of its revenues to the platform stakeholders (notably the token holders)? Yes, 100% to LOOKS stakers

b) x2y2

This NFT platform is a fork of LOOKS with the same Real Yield mechanism on the token. The only notable difference is the implementation of an ETH borrowing service using NFTs as collateral.

However, the platform's growth metrics are impressive, generating more trading volume than LOOKS.

Be careful, though, I may need to be corrected, but in my view, the circulating supply is 600m of token and not 200m as posted on many sites, so the current MC is $51m and not 18.

Nevertheless, x2y2 has excellent metrics and the same virtuous circle as LOOKS. Therefore, it is a good candidate for a long-term NFT and Real Yield market position. Moreover, this marketplace currently offers 35% APY on x2y2 staking:

The P/E of x2y2 is :

Circulating: 51M/19M = 2,68 (not having found the exact number of x2y2 stakes, I have taken into account the total supply in circulation)

Fully diluted: 86M/19M = 4,5

2) Perp DEX

DEXs are undoubtedly one of the most significant use cases of DeFi: they allow users to exchange assets in a decentralized, permissionless, and non-custodial way.

If you are reading this article, I don't think I need to give you examples of centralized organization failures or user abuse in the traditional sphere for you to understand why these three points are so important, especially with the recent Celsius and FTX events we have witnessed in the crypto sphere (which are already reminders of what happened in 2014 with Mt.Gox).

If the potential to rig is there, human beings will take advantage of it'.

DeFi allows us to remove this risk; as the users we must apply the 'Don't trust, verify' famous principle.

So as the crypto market matures, DeFi will grow with it. DEX will even take more and more market share from CEX for several reasons:

Dramatic events like FTX are a good reminder of the usefulness of DeFi; sometimes, we need traumatic events to change our behavior and understand the value of things

DEXs are becoming more innovative, offering features similar to CEXs and even offering some that are not found on CEXs (e.g., the ability to be LP)

The DeFi UX is improving at the infrastructure level, for example, with the rise of L2s, which allow users to benefit from a decentralized environment while having a very good transaction finality (fast and inexpensive), or the Account Abstraction offered by Starknet's @myBraavos and @argentHQ wallets, which provide the same security functionalities and UX as in the web2

The growth potential of DEX compared to CEX is even more true when we check the market shares of these two sectors. In spot trading, DEX only represents 10% of the total market, the remaining 90% being on CEX:

The observation is even more extreme in the Perp market; the three DEX with the highest volume (dYdX, GMX, and GNS) only represent 1.09% of the CEX volume :

If we add the other DEX Perp, we are at around 2%.

In summary, the growth potential of DEX is huge as :

Crypto is small compared to traditional finance

The development of DeFi is still in its infancy

The market share of DEX is tiny compared to CEX

I don't think DEX will flip CEX regarding volume, but a 20/80% or even 30/70% ratio over the next cycle is not a crazy target.

Thus, in the DEX field, there are two types:

Auto Market Markers (AMM)

Perpetual DEX

AMMs were the first to implement the Real Yield principle for LPs, which are rewarded for their liquidity supply by the fees generated by the pools on which they deposit. If you want to know more about how AMM work, I have briefly introduced the topic in 6 tweets here (tweets 2 to 8).

There are many AMM like Uniswap, Sushiswap, Curve, and PancakeSwap. However, I won't go into the details of the AMM, as they are not the most exciting protocols in the Real Yield field. Indeed, they are already highly capitalized, do not necessarily pay Real Yield rewards to the token holders, or have a too high P/E. DEX Perps are more attractive on these three points and have the most growth potential. Moreover, some even offer an AMM Swap service in addition to the Perp one.

In the top 3 dApps with the highest revenues, there are 2 particularly interesting DEX Perp:

If you want to know more about what a Perp is and its importance in the financial markets, I invite you to read this article. On our side, let's look directly at these two protocols.

a) GMX and its forks

GMX is a decentralized spot and perpetual exchange (up to x50) that supports low swap fees and zero price impact trades. I will not focus on its global functioning; I invite you again to read this complete article by Riley if you want to have a detailed analysis of GMX: The complete analysis of GMX.

What is essential to understand in this article is that GMX allows you to swap and execute Perp trades with up to x50 leverage in a non-custodial way on Arbitrum for the following assets: BTC - ETH - LINK - UNI - USDC - USDT - DAI - FRAX ; and on Avalanche for the following ones: BTC - ETH - AVAX - USDC.

In addition, it allows users to deposit liquidity into a multi-asset pool of the assets mentioned above. When you deposit assets into this pool, you get, in proportion to your deposit, GLP, which is an index of assets in that pool. The GLP price varies according to the following formula :

(total worth of assets in the index, including profits and losses of open positions) / (GLP supply)

GMX charges fees for opening and closing positions and executing certain transactions (see the bottom of this page for details of fees). Since its launch, GMX has collected over $150m in fees ($120m on Arbitrum and $30m on Avalanche). Globally, GMX is one of the top 4 revenue generating dApps in the entire crypto market:

Of this revenue, 70% is distributed to the liquidity providers of the GLP pool and 30% to GMX holders:

Considering the innovative reward mechanism of GMX (esGMX and MP), the virtuous circle of this platform is mighty. I invite you to return to part III of this article, in which I explained this virtuous circle.

TLDR: traders have an interest in coming to trade on the platform and holding the platform's token, holders have an interest in doing community marketing about the platform and trading on it, and holders have an interest in compounding their rewards to get more significant share of the platform's fees.

Regarding the P/E of GMX :

Circulating: 520M/69M = 7,54

Fully diluted: 1 030M/69M = 14,9 (but it is essential to take into account that a large part will never be liquid due to the esGMX functioning and that another part will never be stake because it will stay on CEX)

Finally, if we have to answer our famous 4 questions:

Is the project located in an area with a high growth propensity? Yes, for the reasons I stated above (TLDR: growth of crypto and therefore of DeFi, increasing innovation of DEX and UX moving towards CEX, growing importance for non-custodial and permissionless trading so that DEX will take a significant market share from CEX).

Does the project offer a real service that meets real needs? Yes, to be able to trade spot and Perp in a non-custodial and permissionless way, as well as to be able to bring liquidity to the platform and be a 'shareholder'.

Where do the fees/revenues come from, and is the collection model sustainable in the long term? The protocol charges fees for opening, closing, and executing trades, like CEX.

Does the protocol distribute some or all of its revenues to the platform's stakeholders (notably the token holders)? Yes, 70% to GLP holders and 30% to GMX holders

Moreover, in addition to the fact that GMX is located in a sector with a high growth potential, GMX also has many levers to consolidate and increase its market share compared to other DEXs:

Integration of synthetic assets: allowing to have more trading pairs without having intrinsic liquidity problems for each pair; the implementation of synthetics is planned in the GMX roadmap.

Growth of Arbitrum and AVAX: GMX is the leading project in these two chains and will benefit directly from their growth.

Expansion into new chains: this will attract more users and, therefore, more volume and revenue.

Protocols that build on top of GMX: this is already the case, notably with the options and vaults protocols, but it is likely to accelerate with the innovations of DeFi and with the implementation of synthetics.

Due to its success, many forks of GMX have been created on all chains. Let's take a quick look at the P/E of two of them.

Metavault.Trade (MVX) on Polygon:

P/E of MVX :

Circulating: 7M5/440k = 17

Fully: 38M/440k = 86 (but a big part will never be on the market like GMX)

Catalysts for potential individual growth:

Release of a decentralized casino with profits going to MVX holders

Expansion on zkSync

Synthetic assets

Partnership with option protocols on Polygon (like Buffer recently)

Release of an NFT collection

Mummy Finance (MMY) on Fantom:

It is not yet listed on Token Terminal, so let's do the calculation by ourselves:

650,000 (in 84 days) * 0.3 = $195,000 revenue for MMY stakers

195 000*(365/84) = $847,000 annualized revenue

P/E of MMY :

Circulating: 7M1/850k = 8.35

Fully: 9M4/850 = 11

Catalysts for potential individual growth :

Support from the FTM foundation (you can find their address here)

Andre Cronje's return to the FTM ecosystem

Synthetic assets

Partnering with protocols on Fantom

Expansion on other chains

There is a multitude of other GMX forks; here is a pretty complete list:

b) dYdX

dYdX is an order-book DEX built on StarkEx, allowing to trade Perp with leverage up to x20 for BTC/ETH and x10 on all other pairs. It, therefore, allows non-custodial trading without providing any documentation (KYC).

The two advantages of dYdX over GMX are that:

1, it allows traders to trade on 37 different pairs: (BTC, ETH, SOL, MATIC, CRV, NEAR, AVAX, LINK, ATOM, DOGE, SUSHI, SNX, ADA, AAVE, FIL, ALGO, COMP, MKR, XTZ, ICP, LTC, DOT, EOS, 1INCH, YFI, BCH, TRX, ZEC, ZRX, UNI, XMR, ENJ, CELO, RUNE, XLM, ETC, and UMA). At the same time, on GMX, it is currently only possible to trade on 5 assets.

2, dYdX has colossal financial resources to build its DEX and benefits from the network and advice of top VCs, as they have raised $87M from the VCs below:

This DEX, therefore, clearly has the arguments to establish itself in the Perp DEX landscape for the long run. Notably, if you look closely at the metrics, dYdX is the second-highest revenue-generating dApp, just behind OpenSea and ahead of GMX:

These revenues come from the trading fees of the platform's traders. I invite you to go here for more information about the dYdX fees.

The issue with dYdX in this Real Yield essay is that this DEX does not distribute the revenue it generates to the dYdX token holders. In addition, the token only serves the purpose of governance and a fee reduction. There needs to be more to compensate for the liquidity mining of the token and its high inflation. For information, dYdX refunds a large part of the traders' fees by distributing the dYdX token to them (according to the volume of each trader in proportion to the total volume).

This high token inflation, coupled with the low utility given to holders, has led to the price falling. In addition, there are large unlocks weighing on the project at the end of 2023:

However, the V4 of dYdX, whose Mainnet is planned for September 2023, will enormously change the token's utility because this V4 intends to launch a sovereign dYdX chain on Cosmos, giving much more utility to the token and allowing the project to become 100% decentralized. At the token level, as soon as this V4 is in place, the token will keep the same utilities as before (governance and fee reduction), but new ones will be added, notably the security of the dYdX blockchain, which will be achieved through the staking of dYdX. In exchange, stakers and validators will receive the fees generated by the platform (real yield):

One application of this is that traders would not pay gas fees to trade, but rather pay fees based on trades executed similar to dYdX V3 and centralized exchanges. These fees would accrue to validators and their stakers.

The revenues generated by dYdX are pretty impressive, we are talking about more than $100m per year.

If we calculate the future P/E of dYdX, we have the following:

Circulating: 450m/105m = 4.2

Fully: 3 000m/105m = 28.5

Returning to our four questions:

Is the project located in an area with a high growth propensity? Yes, for the reasons I stated above (TLDR: growth of crypto and therefore of DeFi, increasing innovation of DEX and UX moving towards CEX, growing importance for non-custodial and permissionless trading, so DEX will take a big market share from CEX).

Does the project offer a real service that meets real needs? Yes, the ability to trade Perp on 37 pairs in a non-custodial way.

Where do the fees/revenues come from, and is the collection model sustainable in the long run? The protocol charges fees on trade opening (makers' fees being lower than takers' fees).

Does the protocol distribute some or all of its revenues to the platform's stakeholders (notably the token holders)? Not yet, but it plans to do so as soon as the V4 is released (in September 2023).

On an individual level, dYdX has many catalysts for potential market share growth:

Creation and migration to its own Cosmos sovereign channel

Partnerships and integrations of dYdX with other Cosmos chains

New tokenomics and implementation of a real yield mechanism

Integration of more trading pairs

NFA, I find this asset very interesting in a few months horizon, but I will be very wary about the big unlock planned in December 2023.

There are other areas where this real yield innovation is relevant, such as options or liquid staking, but I need to learn more about these domains to write an article about them. I will do a dedicated article if you are interested when I am up to date.

VI/ Starknet projects that will (or should) include this mechanism

As Starknet is still in an early development phase, its DeFi ecosystem is minimal; only some dApps are in Mainnet so far.

It is, therefore, challenging to say. Nevertheless, three projects have already announced that they want to integrate a real yield mechanism. We can also extrapolate by identifying projects with interest in implementing it. Let's see now.

Reminder: this is an introduction to these projects; I plan to make threads and detailed articles about each soon.

ZKX

ZKX is a derivatives protocol based on perpetual swaps. This innovative Perp DEX has already announced the upcoming release of a token with a Real Yield mechanism attached. Here are some of the innovations that this project will offer:

Liquid gouvernance : Governance will no longer depend solely on the number of tokens a person holds but on what users do on the platform, thanks to the virtual governance share (VGS) introduction. In other words, the more actions a user performs on the platform, the more VGS he accumulates. Knowing that the VGS will decrease over time; therefore, if a user does not participate anymore, he will gradually lose his VGS

Creation of its own decentralized limit order book (DLOB) : ZKX will implement a decentralized and permissionless nodes network with its own consensus and data availability layer

Swap Liquidity Mining in ERC-20 : ZKX is creating an incentive system that allows DAO and projects to provide rewards for the trading of swaps within the ZKX protocol

ZKX is also working on many others, such as the Adaptive Balancing Rate, T-Swap, or an incentive mechanism offering premiums on the riskiest assets for traders to maintain balance and liquidity. We will discuss this in more detail in a future article.

To best build its protocol, ZKX has raised $4.5m from the following VCs:

I strongly advise you to follow this project closely because :

It will benefit from the Perp Dex market’s growth

It is one of Starknet's most innovative projects and one of the only ones to have raised funds on it

It offers many innovations

It plans to integrate a Real Yield mechanism backed by its token

zkLend

zkLend is an innovative money market built on Starknet, which aims to create two distinct products:

Artemis for traditional DeFi users

Apollo for institutional users

If you want to know more about this project, I have already wrote a presentation thread, which you can find here.

The important thing to remember about zkLend is that they raised $5M to build their protocol, making it one of the only Starknet protocols to have raised funds to date. In addition, they are planning to include a real yield mechanism on their future token:

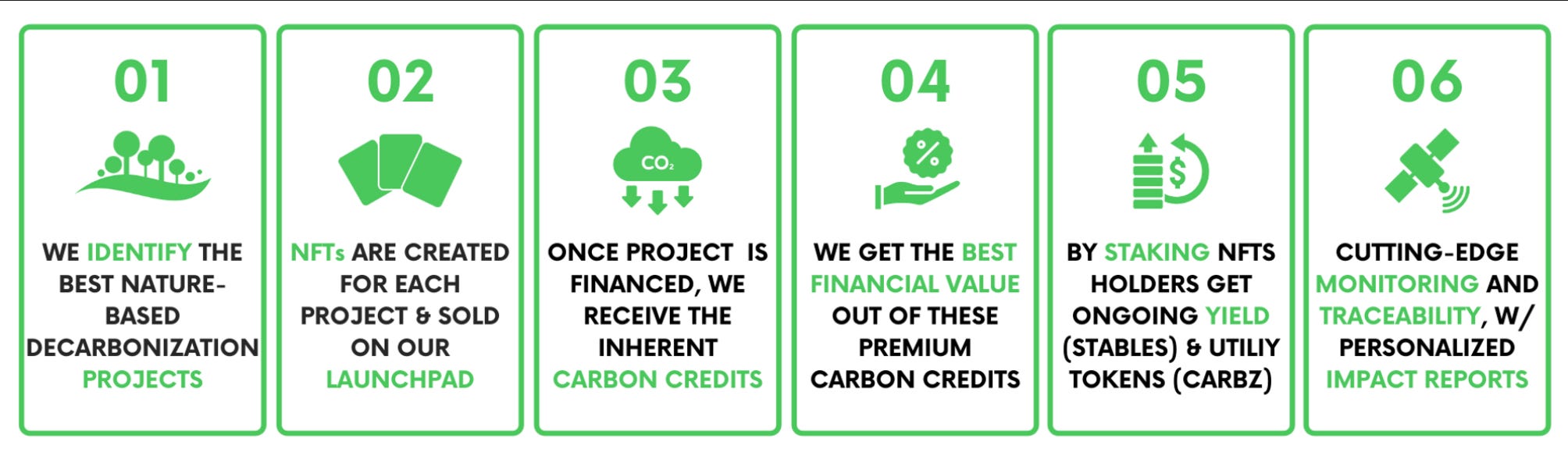

Carbonable

The innovative DeFi project allows investors to invest in projects that contribute to the preservation of our planet in the form of NFTs. Their primary goal is to participate in the decarbonization of the earth.

An ethical and remunerative project mixed with crypto and NFT; beautiful, isn't it?

The project is quite simple: the Carbonable team selects the best projects to decarbonize the planet, then lists them on their launchpad as NFTs, and the NFT holders receive a passive income.

The beauty of this project is that they don't need tokens to operate. So you can now receive a real yield by buying their first collection or investing in future Carbonable NFT collections on their launchpad. However, a token is not out of the question, and including a real yield mechanism on it would be easy.

Again, stay tuned, I'm planning to do full coverage articles on these three projects soon.

For the other projects, let's speculate.

NFT marketplaces :

There are two NFT marketplaces on Starknet and another one that will be launched soon. Regarding the live ones (in Mainnet and Testnet), we have:

Aspect, which is Starknet-focused

Mint Square, which is multi-chain (zkSync and Starknet)

In addition, there is Moso, which aims to create an innovative NFT marketplace and plans to launch its Testnet soon.

None of these three projects have announced tokens or tokenomics, but they will likely release one. If they do it, it is in their interest to create a real yield system like Looks and x2y2, but also come up with some adjustments to overcome the big inflation rate at the beginning and the collapse of the token value.

DEX

Let's start with AMM. There is a multitude of AMM building on Starknet. Currently, the only three lives on Mainnet are:

Others currently live on Testnet:

We have no information about future tokenomics for these AMM, but we can hope that at least one of them will include a real yield mechanism. If I had to choose only one, my bet would be JediSwap, knowing how community-oriented this project is.

Regarding order-book DEX, we have:

Brine for spot trading

Sphinx for cross-chain trading

ZKEX, the multi-chain DEX focused on ZK (zkLink, Starknet, zkSync)

Mes protocol, the multi-chain DEX competitor to ZKEX, which is also focused on ZK (zkSync, Starknet, Polygon zkEVM)

These DEXs have not made any token announcements to date, except that ZKEX seems to be looking to implement a mechanism that attracts users in the long term:

ZigZag and Rabbit are also DEXs that plan to deploy on Starknet, but they already have a token, and both tokens do not include a real yield mechanism:

Money Market

Then we have Money Markets. As presented above, zkLend already plans to include the real yield mechanism. We have no information yet for the other Money Markets. Nevertheless, it is interesting to follow them to see if they will include it or not:

Nostra, which in addition to its Money Market is building an AMM and the first Starknet native stablecoin (UNO)

Hashstack, the under-collateralized money market

Curve Zero, the fixed interest rate money market

Others

In fact, all projects that charge fees can include a real yield mechanism in their tokenomics, creating a virtuous circle around the project while rewarding all stakeholders. Therefore, we can also mention in this article :

Starknet_ID, which is the equivalent of ENS on Starknet. As a reminder, ENS's annualised revenue is $20M

Carmine, the AMM for options, which allows to buy and sell European-style options

Conclusion

In conclusion, the Real Yield mechanism is probably the most accessible DeFi mechanism to understand. Warren Buffet has already demonstrated the importance of investing in sectors and projects you understand through his success. This is even more important in a sector as complex as crypto. In this sea of technology and complex mathematics, it is indeed easy to analyze the financial metrics a protocol generates and how much of the protocol revenue goes to the holders. You just need access to these metrics and understand the tokenomics of the project and the sector in which it is positioned.

Ultimately, this narrative is here to stay for the long run: the real yield mechanism is already established in the traditional financial world and has already shown how well it works. By incorporating Real Yield into DeFi, we get a mix of two worlds: the traditional financial world, using the mechanisms that have already proved their efficiency, and the DeFi world, allowing to counteract the failures of this first world.

The exciting part of all this? We are only at the beginning of this sector.

If you enjoyed this article, feel free to share it and follow me on Twitter; that's the best way you can support me and push me to continue. Also, feel free to subscribe to this Substack, it’s free !

Thank for this article.